Some people are lucky enough to be given a gift by a family member. A lot of times, the recipient doesn’t even know too much about what the inheritance is, or how to begin deciding what to do with it.

We can go into more detail about several types of inheritances another time. Let’s assume this inheritance is in stocks or semi-liquid assets. A lot of people who receive an inheritance are anxious about its concentration. It could be in only one or two stocks, it could be a single real estate property.

Depending on your level of confidence in managing investments, there are multiple ways to approach your new inheritance. In my mind, the number one goal is to be comfortable with your investments.

The Bottom Line

I’m a big advocate of investing as much of your inheritance as you can while being realistic with any large financial commitments that are coming up. Planning on going to grad school soon? Maybe keep a little of that inheritance in a savings account so you can easily access it and avoid paying capital gains taxes.

You should be investing around 80% of your inheritance. The other 20% can be split between saving for a big purchase and adding to your emergency fund. The more money you can have working for you the easier it will be to lead a financially freeing life.

Goal setting is essential to putting together your career and investment decisions. Good goals share a couple of common characteristics.

I’m a person who always has big plans but has trouble following through. When I was a kid playing chess I’d have great opening moves but I would never close the game. Understanding your tendencies and weaknesses is essential to put yourself on the correct path to achieving your goal.

Specificity should be front and center when thinking about career & investing. Usually, those goals are monetary. If you have a goal to live a certain lifestyle, what amount of capital do you need to acquire to live that way?

Setting a specific dollar amount is a great goal because it is clearly articulated and measured. It doesn’t do much good to say, “I want to be rich” or “I want to be financially independent”. If you have a number you can work toward, that makes the journey much more realistic.

Time Constraints

If you never set a date at which you’d like to achieve your goal it’s doubtful that you’ll ever achieve it. Specificity combined with a time constraint allows you to break up your goal into manageable chunks.

Think of a longer time horizon, and set your goals to be big. Then start to break them into yearly goals. It’s better to dream big and fall short than be too conservative. Our world rewards risk takers and dreamers.

The End Goal

It’s important to have a purpose in mind for saving and investing. A lifestyle you want to live, the flexibility to take a job you actually want, the ability to pay for your children’s education, whatever it is find something that motivates you.

For myself, I want to be able to do whatever I want to do without fear of ever “needing” a job. I never want to be in a position where I’m forced to stay in a job that I’d like to leave. Hoarding capital allows you the ultimate freedom to do as you desire.

Take a couple of minutes to listen to Buffett, I think it’s important to not be taken away by excess.

Here’s an example of some possible goal setting for an ambitious investor:

Goals: Net Worth $1,000,000 by December 1, 2035 Save $75,000 for graduate school by February 1, 2025 Earn $100,000 yearly income by December 1, 2029 Be Self Employed by December 1, 2035

It could be easier to substitute years for your age, but any way you tweak these basic goals should help you out.

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

Ben Graham, the famous investor known for mentoring Warren Buffett and advocating for value investing, had a couple of brief rules for allocating your portfolio funds.

He has a simple rule depending on if you are an enterprising or a defensive investor.

How do you determine if you’re an enterprising or a defensive investor?

It’s not down to your age, but instead how much time you’re willing to put into managing your portfolio.

Enterprising vs. Defensive Investing

If you can’t really be bothered to take the time to properly value companies and invest in them, you’re a defensive investor.

You want to see your investments grow modestly without much effort.

If you get a lot of enjoyment from valuing companies and you want to spend the time to make these decisions in your portfolio then you’re classified as an enterprising investor.

Portfolio Allocations

Ben Graham advises that the enterprising investor limit his portfolio allocation to 75% in equities and 25% in bonds.

He advises that you never hold less than 25% of either bonds or equities.

You can rebalance your portfolio to be more or less conservative.

Graham’s argument for holding 25% of your portfolios in bonds is that it would give you the confidence to stay in the market whenever there is a market downturn.

An important note is that when Graham was writing his various editions of The Intelligent Investor US Treasury bonds were returning much more than they are today.

Portfolio diversity is an admission that you can’t select winning companies to invest in, which is okay.

Not everyone wants to dedicate the time and effort to learn how to evaluate companies and then consistently monitor them for investment opportunities.

But look at Buffett’s advice. Even when you buy the entire market through an index fund, he claims it’s best to place 90% of your portfolio in that one fund.

Sometimes diversifying can detract from our overall returns, especially if we diversify into high-cost equity funds.

How is your portfolio allocated? Would you consider yourself a defensive or enterprising investor?

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

A lot of people don’t save to invest their money. To be honest it goes against most peoples’ nature.

Living within your means is difficult. Especially now with all of the advertising we are bombarded with every day.

It’s difficult to save and invest. We have to give up those shoes we want or a couple of dinners at that restaurant we really like.

It is guaranteed that you’ll have to cut your budgets in some areas to invest money.

Sometimes it can feel like a chore to sacrifice things now. To save some of the money you work hard for and not use it on yourself.

The big question is why do we save to invest? What is the purpose?

Why Do We Invest?

We Want To Be Our Own Boss

We save because if you’re like me, you don’t want to work for someone else for your entire life.

When you have a salary and no other sources of income, you become much more dependent on your job.

We save because one day we don’t want to have to punch the clock or get up extra early for that meeting someone else set.

We want the financial independence that comes with investing so that we can make our own decisions and do what we want to do.

We Want The Option To Quit

Sometimes we’re treated unfairly at work. Other times we’re asked to take on responsibilities we’d rather not.

If you don’t have a safety net built from your investments then you really don’t have an option other than to comply in your current job or find a new one.

Often we enjoy our work and want to keep working. We don’t need financial independence immediately so that we can quit.

Rather, we want financial independence for the mental relief it offers.

We would all feel a lot better about going to work if we knew we didn’t have to.

We Want To Be Wealthy

Let’s be honest, no one gets wealthy from living off of a salary. Those executives who get millions of dollars in salaries have outside investments as well.

If you want to build wealth then you need to save your money and invest.

That can be in the stock market or a market you’re more knowledgeable about.

Maybe you have an eye for art and want to collect original pieces.

You love classic cars and appreciate that the right ones can actually increase in value, unlike most new cars.

Maybe you’d love to have your own business one day, and you’re waiting for the right one to come available so you can purchase it.

You need liquidity in all these situations. You won’t be able to invest in what you want unless you have money saved and prepared to invest when the time is right.

We Don’t Want To Work Forever

Even if we enjoy our jobs now, there will be a time when we would rather pursue other things than our careers.

When you grow older spending time with your family and kids may become more pressing than getting your next promotion.

When your priorities change you want to have the financial independence and flexibility to adjust your life accordingly.

Unless you’ve found your dream career you can do until you die, most of us think we’d like to retire early and spend time pursuing hobbies or crossing items off our bucket list.

Once again, we need the income from the investments we’ve made over our life to realize these dreams. None of this is possible without being financially independent.

Investing becomes easier once you have a goal in mind. Proper preparation can make difficult tasks become so much easier.

Why do you save money? What are you investing in now? What are your investing goals? Let me know in the comments below.

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

Recently I watched a David Rubenstein interview with the successful venture capital founder & investor Marc Andreessen. I watched the later half which mainly focused on Andreessen’s investment advice.

I’ve enjoyed Rubenstein’s interviews but this one stood out to me immediately. I caught it again a couple of days later on TV and I realized what made the interview stick out in my mind.

Rubenstein has a very serious personality interspersed with bits of dry humor. Andreessen on the other hand is extremely lively and chuckles at his own jokes. The two could not be more different in their personalities but they are both incredibly successful businessmen.

Andreessen had some interesting investing advice he revealed in this interview. Before I get into the advice itself I want to add a little background to who Rubenstein & Andreessen are, and what they’re known for.

The Carlyle Group has since grown to manage $260 billion and has 29 offices around the world.

He is a published author and currently hosts The David Rubenstein Show: Peer-to-Peer Conversations on Bloomberg & PBS.

He is an avid historian and owns rare copies of some famous legal and historical documents such as the Magna Carta, the Declaration of Independence, and the U.S. Constitution.

Rubenstein typically interviews influential business leaders on his show that are well known or attempting to do extraordinary things. His show gives us an insight into the lives and thoughts of these people.

What makes his interviews so interesting is that he is more of a peer than just a professional journalist. This adds another layer to the interview that usually isn’t present when most professional journalists obtain interviews.

Marc Andreessen

Andreessen is an influential billionaire venture capitalist investor. He got his start in tech by co-founding Netscape along with other important early internet companies before they became acquired by larger companies.

a16z has funded companies such as Twitter, Facebook, GitHub, Airbnb, and many more.

Part of the reason that Andreessen has been so successful is that he has experience founding companies and the founders he invests in respect that.

He also mentioned multiple times in the interview with Rubenstein that he is in the relationship business, and you can tell he is extremely personable.

Private Equity & Venture Capital

These two businessmen are both active in the world of finance, albeit in slightly different ways. Venture capital and private equity are very similar but have important distinctions.

Private Equity

Private equity is when investors purchase equity in a company privately, in other words not through the stock market.

Think of it as a direct transaction with the company you are purchasing equity from. Private equity is interested in beating the market and generating sizable returns.

They are usually interested in more stable companies that may have a reason for wanting to remain private, including not having to answer to public shareholders. Another reason firms invest may be that they see a way to grow the business’s revenues and make their equity share more valuable.

Furthermore, these companies are no longer considered start-up companies. These are more mature and stable companies, I like to think of the distinction as fewer engineers leading and more MBAs.

Venture Capital

Venture Capital investors have the same idea as private equity investors but they target different companies. VCs target startup companies, from early stage to late stage companies.

Startups need VC money to grow their company and build their products because their business is not generating significant cash flow yet. You’ll see that technology is one of the most popular industries to invest in at the VC level because of its scalability and user stickiness.

Investment Advice From Marc Andreessen

At one point in the interview, Rubenstein starts asking questions about investing and getting Andreessen to give his take on investing decisions. Andreessen had some interesting answers to the following questions.

I think this is great investing advice for someone who wants to invest but maybe doesn’t have the confidence to pick and choose specific ETFs or stocks.

How Do I Invest With A Good Venture Capital Firm?

Surely a great VC like Andreessen would have some tips and tricks for investing with top VC firms, right? Think again.

MA: “The venture capital firms that are open for outside money are generally the ones you don’t want to invest in”.

The top-tier VC firms that make 20%-40% returns on their money are not open to the general public. They are open to very wealthy individuals with connections to the industry who have a lot of capital to put forward into a VC fund.

What’s The Best Investment Advice You’ve Ever Received?

MA:“It’s probably from Warren Buffett. Put all your eggs in one basket and watch that basket. Really know what you’re doing. Really deeply understand the nature of what you’re investing in”.

Warren Buffett is famous for being one of the most successful investors of all time. He understands his company’s business model, its industry, and its customers as well as the CEO running the business.

Invest your money into companies that you know inside and out, speculative investing is a sure way for you to lose money in the long run.

What’s The Most Common Investment Mistake You Observe?

MA:“I think it’s the opposite of [putting all your eggs in one basket and watch that basket]. I think it’s when people read something in the paper or see it on TV and they take a flyer on it without really understanding it”.

This correlates with speculative investing. Investing in a business because it’s hot right now without understanding the business and its goals and its customers will surely lose you money in the long term.

It’s important to do your due diligence before investing. We want to grow our wealth not gamble with it!

If I gave you $100,000 tomorrow what would you do with it?

MA: “I’d put it in an S&P 500 index fund. Don’t get fancy”.

If you are investing in the public markets it is very difficult to outperform the S&P 500 in the long run. Those 500 companies are some of the best companies in the world and with an index fund, you have an equity stake in them.

Even many professional investors agree that with smaller amounts of capital it’s generally a solid idea to track the public markets instead of actively trying to beat them.

Time will tell if Kathy Woods’ ARK funds will end up proving that popular investing philosophy wrong.

Keep Things Simple

What does all of this mean for us? It pays to keep investments simple.

Have fun with your portfolio, really research the individual companies you choose to invest in, and follow their quarterly earnings and shareholder letters. Andreessen’s investment advice is to become an active equity investor.

At the same time, it’s probably a good idea to keep the majority of your money in an S&P index fund for long-term growth.

VC and PE investors have access to amounts of capital we don’t and therefore they have the ability to purchase meaningful equity in private markets and they have the ability to realize much greater gains than in the public market.

Until we reach that level of wealth. Keep things simple and invest abnormally.

Do you agree with my conclusions? What do you make of Andresseen’s advice? Any thought on private equity or venture capital? Let me know in the comments!

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

Even though many places in the world are still feeling the effects of COVID-19, the US stock market has seen tremendous growth.

Performance of the US Stock Market in the past year

After hitting a low of around 26,500 points in late October, it has rebounded up to 35,000 points as of today.

Keep in mind that all of this happened during great times of uncertainty and restrictions being imposed in many places around the world.

The continual surge of the market even during these times tells me that companies and money managers are confident that the worst of the pandemic is behind us.

Recent Earnings Beats

Some companies have really beaten their earnings estimates this quarter.

It’s telling to look at the industries these companies are in because it’s a good indicator of what consumers are spending their money on.

Here’s an example of two companies that stood out.

Ralph Lauren

Take Ralph Lauren (RL) for example. The earnings estimates were $0.89 EPS, but RL recorded $2.29 EPS.

There are some other interesting notes from their earnings report. Their digital e-commerce capabilities saw an 80% growth YOY.

Ralph Lauren achieved their highest gross margin since 2014. Revenue is expected to grow 25%-30% as in the next year.

In Q2 RL’s net revenue increased 176%. Including a 278% increase in physical stores and a 51% increase on their digital platforms.

These strong performance metrics don’t signal a consumer base that believe they will be staying inside and quarantined for work.

This means that many people receiving signs that even if they won’t be returning to the office full time that they are expecting to go out and dress up.

Spirit

Spirit (SAVE) is a budget airline operator that prides itself on being a low cost choice for people who want a vacation.

These figures are adjusted EBITDA earnings per year, which leaves out cash flow activities that are invested back into the company to generate positive future cash flows.

Some of the investments Spirit is making include investing in new routes to accommodate increasing south Florida travel.

Spirit is making investments because more people are traveling now and looking to travel in the future. A good sign for the markets going forward.

Consumer Market Sentiment

I believe these earnings beats and the general upward trend of the market are the result of a couple of possibilities.

Consumers Are Spending At Normal Levels

In some states especially in the Southeast United States, there are little to no lockdowns or restrictions. I would say most consumers in these regions are spending how they spent before the pandemic began.

These consumers are probably contributing to some of the overall positive consumer sentiment, especially in popular vacation locations such as Florida.

However this region is not reflective of the entire nation, and it is a different story in other areas in the United States.

Consumers Are Expecting To Spend At Normal Levels Soon

In other areas where gatherings are still more restricted, the e-commerce capabilities of almost every consumer retail brand has allowed consumers to continue spending on things like clothing.

This is in spite of the fact that their areas might be under restriction.

A big sign of this is Ralph Lauren’s e-commerce growth that I mentioned above.

Consumers are spending with the expectation that their lives will be make to normal sooner rather than later.

They have faith that most restrictions will be lifted and they will be able to spend their money where they want and go where they want.

You don’t buy more Ralph Lauren clothes if you are expecting to stay in and never go out to restaurants or bars or parties.

Consumers Plan To Disregard Restrictions Or They Spend To Feel Better

The last assumption can go either way.

Consumers might be tired of restrictions and plan to go about their normal lives in places that don’t follow the restrictions.

Another option is that consumers are buying more clothes as a way to cope with the fact that they believe restrictions will continue due to the Delta variant.

Think of this a little bit of retail therapy.

I think all of these possibilities are potentially true, and there are probably consumers who are behaving in all of the ways I discussed.

At the end of the day it doesn’t really matter why consumers are spending more, it is beneficial to the markets that consumers are spending more.

Where Is This Spending Power Coming From?

Where is all of this discretionary consumer spending coming from during a pandemic?

They found that the savings rate has stayed around 14% since April 2020. Americans have been saving a lot more during this pandemic and are eager to spend it.

Federal Stimulus

Let’s assume that the average American family is a couple with two kids and a household income of $70,000.

A grand total of $11,400 would have been given to this average family during this pandemic.

Theres no doubt some of this as gone to essentials such as rent and food, but the government’s reason for direct relief was to stimulate the economy and prevent a recession.

If the broader economy is stimulated, it makes sense that the market will usually follow suit.

There is no doubt a chunk of this relief has gone towards consumer discretionary items, combined with the higher savings rates can attribute to the extra cash a lot of consumers seem to have during this pandemic.

What do you think about the upward trend of the stock market? Are companies and consumers being too bullish? Or do you think they’re bearish and I got the analysis wrong? Let me know in the comments.

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

You have time to incur losses and bounce back, so a reasonably aggressive approach would benefit your portfolio better.

Some Fund Managers Do Beat The Market

40% of managers do beat the market! That’s a large amount of funds to choose from.

Invest in these funds!

Do your research and identify the funds that regularly beat the market.

Keep in mind that past performance is not indicative of future results.

Anything can happen to your funds, and there is not a guarantee that any fund will continue to under or over perform the market.

Take the ARK funds as a recent example of a fund’s fortunes changing drastically.

It’s innovation fund TICKER: ARKK is down -17.94% at the time of writing compared to the S&P 500 index which is up +17.74% year-to-date.

Take the time to do your research and keep the amount of risk you’re taking on in mind.

Do not forget to check the fees that funds charge.

Funds that aim to beat the market often have huge fees, only to underperform a cheap index fund.

Actively Managing Your Own Investment Fund

Some people treat their investment accounts as their own fund.

They trade individual stocks and options instead of mutual funds & indexes.

This is obviously the most risky way to manage your money, as individual stocks are prone to much greater movements than larger funds.

Most people do not diversify enough with their individual holdings which leaves them overexposed in some industries and lacking exposure in others.

Mad Money Advice

Jim Cramer has solid advice on how to structure your investment account.

He suggests on investing your first $10,000 into a low cost index fund.

It’s important to look at a fund’s prospectus to understand the fees they charge, and also look at fee that your trading platform has on funds.

TD Ameritrade has a $49.99 charge on No-Load mutual funds as an example, which isn’t a big deal if you’re investing a couple grand but it is if you invest a couple hundred dollars.

After building up $10,000 in your index fund Cramer suggests keeping around 10 diversified individual stocks in your portfolio.

He claims this is a manageable number of companies that allows you to still keep up with quarterly and annual reports.

Options Trading

Options can get a little tricky, but there are two basic forms of options. Calls and puts.

Calls give you the option to purchase (call) or sell (put) a stock at an established price by a set deadline.

So with these options, its beneficial for you is a stock’s price increases with a call, since before the increase you’ve locked in a purchase price.

You essentially have the right to purchase shares for a discount from their market price.

The opposite is true with puts. You stand to benefit if a stock’s price goes down because you have the right to sell the stock for a price that is higher than it’s current market price.

A lot of trading of options happen, but it’s common for options to not actually be executed.

Options Trading Is Risky

For most part-time investors options are too risky of a strategy to effectively execute.

I would say they are one of the riskiest strategies available to most investors.

I got burned with options after initially having some success with them.

It’s important to remember that us casual investors are woefully under-informed compared to the massive institutions that execute thousands of complicated trades every day.

If you are interested in options make sure to do your research and really understand the risks.

Meme Stocks

You might have heard about “meme stocks” during the past year. One of the biggest has been AMC.

AMC was in financial trouble during the pandemic because lockdown restrictions were impacting their business model.

What short sellers were hoping would happen to AMC

Investors on Reddit saw that many of the large hedge funds and money managers were shorting (buying puts) on AMC.

Many of these Reddit investors were avid AMC customers, and were determined to not let their favorite movie theater franchise go out of business.

They started buying AMC en masse which drove the price of AMC up and screwed the short sellers because they now held options that were essentially worthless.

They had the option to sell AMC at a price that was below the market price, which of course no one wanted to exercise or buy the options.

What do you think? Do you prefer active or passive investment funds? Do you trade individual stocks? Are options a good long-term strategy? Let me know in the comments

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

But I don’t like paying rent at all! In fact the sooner I can be in a position where I don’t pay rent, the better.

That’s why my immediate medium-term goal is to invest in a piece of property that I can live in and rent out the additional space I don’t use.

I could do this with a house, but I really don’t want to bother living with roommates. They’re bad enough as roommates so I can’t imagine having to deal with them as a tenant.

That’s why most of the properties I’m interested in are multi-family units.

Think duplexes or condos.

That way it’s possible to live in one unit and rent out the other to a prospective tenant.

If I plan it right the rent from one unit could pay my mortgage & utilities! Let’s look at example.

How Does House Hacking Work?

Usually when you buy an investment property you have to put 20% down to avoid expensive mortgage insurance and to qualify for a loan.

That rule doesn’t apply to house hacking, because your investment property is also your primary residence.

This means you can qualify for a loan with much less that 20% down because you are buying your primary residence.

Think about how much that changes the investment strategy now. Let’s say the properties I was looking at investing in were between $300,00 – $400,000.

That would usually mean a 20% downpayment would require $60,000 – $80,000. There are several federal programs for 1st time home buyers where you can qualify with as little as 3% down.

That means you can qualify for loans with between $9,000 – $12,000. That’s a much more attainable downpayment.

It’s important to note that you still have to pay for the mortgage insurance if you put down less than 20%.

Another disadvantage of putting less money down is that your monthly payments will be higher.

The key here is to make sure that the rent you can charge on the other unit(s) is equal to or greater than your payment. This is usually easier when your multi-family property has three or more units.

I think a duplex is a great starting point for house hacking. They’re cheaper than larger units and you can pay a little more and get a pretty nice duplex to live in.

Choosing A Mortgage Loan for Your Property

There are three common lengths of mortgages when purchasing real estate. 30 years, 20 years, and 15 years. The longer the mortgage the lower the monthly payments will be.

The only problem is you end up paying more in interest over the life of your loan.

There are more complicated loans than the three I’ll talk about here like the 7/1 ARM loan.

For now I’m going to focus on three simple loans that make it easy to understand the benefit of buying multi-family real estate for your primary residence while renting out the other units.

I’ll demonstrate the 30-year mortgage in detail and then compile the rest of the information in a comprehensive table.

I’ll reference graphics from bankrate that illustrates how much you’ll pay in interest for the three loan types.

30-Year Fixed Mortgage

All of these mortgages we are considering should be fixed, which means you lock in the current interest rate for the length of the loan.

This is a no-brainer because right now most rates are just under 3% which is dirt cheap.

If your target property is $400,000 here is what your cash flow could look like with 20% down or 3% down.

I’m assuming this $400,000 property is a duplex with each unit having two bedrooms and one bathroom.

The monthly payments are not outrageous, those would be pretty common rents for a two bedroom and one bath apartment. The Maintenance costs included cover any repairs you might have to make as the landlord.

Living in one unit and renting the other out for $1,900/month would leave you with a $52 payment to cover the mortgage if you put 20% down, and $333 to pay if you put 3% down.

This is where the magic starts to happen.

That amount you pay is basically your rent.

I don’t know anywhere in a large metro area where you can rent a two bedroom unit for that amount with NO roommates!

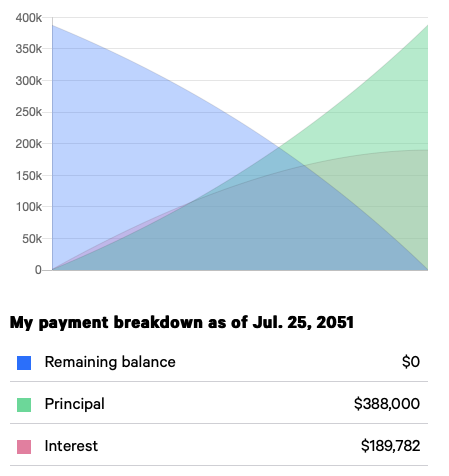

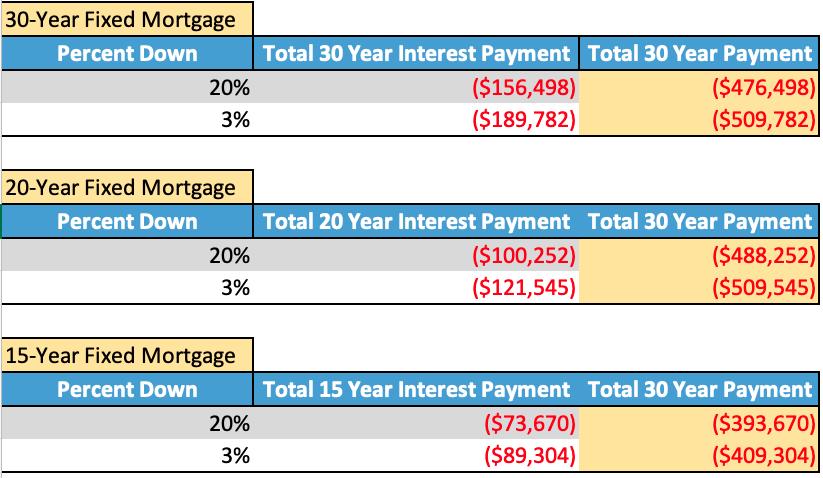

Let’s see how much you pay in interest over 30 years with 3% down:

After 30 years you’ll have paid $388,000 in principle and $190,000 in interest. That brings the total amount paid for a $400,000 property to roughly $578,000.

Essentially you pay a premium of $178,000 over 30 years because you don’t have buy the property for full price.

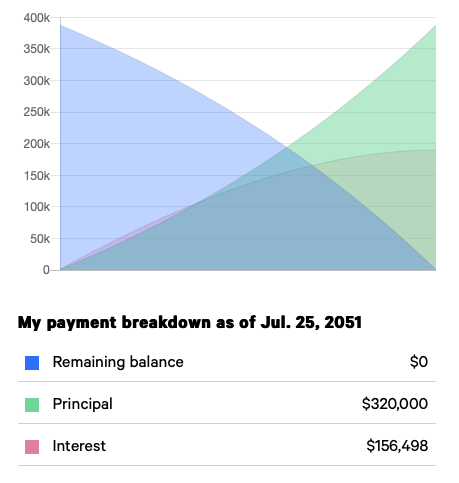

Compared to the loan payment with 20% down:

You already see that you pay less interest over 30 years, because you’re not borrowing as much money. You pay a total of roughly $476,000 in total on a $400,000 property.

This is a much more attractive payment plan than financing with only 3% down. The downside is of course that it requires more initial capital.

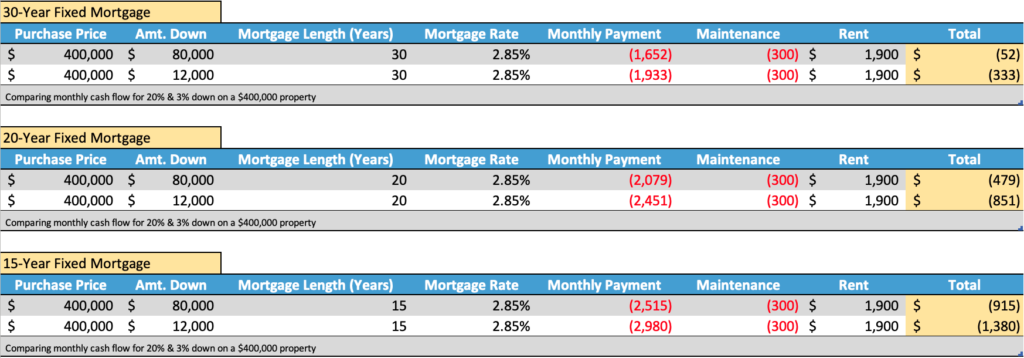

To save you the time of looking through two more sections of this, check out this compiled table below.

Compiled Mortgage Payment Tables

Here is what your cash flow would look like for each mortgage scenario. This also takes into account if you would rather put 20% down or 3% down.

Compiled table of monthly cash flows for 30, 20, & 15 year fixed rate mortgages

The highest monthly payment you could have is in a 15-year mortgage with 3% down.

$1,380/month is equal to rent for a nice one bedroom unit in my area so that’s a good deal.

However, it’s not really the best because we want to lower our living expenses with house hacking.

This makes the 20-year mortgages look like the best deal, especially if you can put 20% down.

Before we come to any conclusions we should compare the total amount paid for each loan, especially looking at interest.

Total interest & principle paid on 30, 20, and 15 year fixed loans

Knowing that monthly payments are cheaper with longer loans, you might be tempted to opt for the longest loan.

But looking at the above table, you see you’ll actually pay the most in interest with a 30 year loan and 3% down.

It comes as no surprise that the cheapest loan is the one for the shortest amount of time and the most money down.

Keep your total costs in mind when financing your property. I am fairly debt-adverse so I feel more comfortable with the idea of a 20 or 15 year loan.

Paying Off Debt With Inflated Dollars

Although you might argue if you want to never sell income producing properties why does it matter how long your loan is?

There’s one more aspect that I have to mention before talking about taxes.

Remember when I said that it’s important all of these loans are fixed?

That’s because not only do you lock in historically low interest rates for the duration of the loan, but you are paying down your debt with inflated dollars.

Think about it this way, when you lock a loan in, you guarantee that all of the loan fees and interest you pay are on present dollars.

So if you take out a mortgage tomorrow and lock in the rate, that’s a rate and a repayment schedule of 2021 dollars.

In ten or twenty years your salary could have increased 2-3% per because of inflation.

So whereas you were paying off your debt with a salary of $100,000 in 2021, in 2031 you’re now paying off the same debt with a salary of roughly $135,000.

That’s not even accounting for all the raises you’ll receive over ten years!

Essentially you’ll have more money to pay off your debt thanks to inflation.

Paying yesterdays debt with todays dollars is almost always a good idea, because inflation is trending up.

All of the benefits I’ve mentioned so far only get better and more pronounced if you buy larger properties with more units.

It all depends on the area you live in and the prices, but you can conceivably turn a profit if you purchase a quadplex instead of a duplex.

Inflation Impacts Your Property Value

Using the same rate of inflation of 3% for home prices (although in 2021 home prices have increased much more than 3%) we can see the value of your property in 10 years.

The $400,000 property you purchase today will be worth almost $538,000 in 10 years.

After 10 years with a 20-Year fixed loan and 20% down you’ve paid off roughly $140,000 in principle and have roughly $178,000 in principle left to pay down.

So you’ll have $360,000 in equity after 10 years, and you’ve been paying $479/month towards the mortgage.

This is basically magic, and I’m not even including rent increases due to inflation!

Now you can see why investing in real estate is so popular for the wealthy, if you buy smart you’re almost guaranteed to make money in the long term.

Tax Benefits

When you invest in real estate you get access to certain tax privileges.

Some of the most attractive deductions include the ability to deduct property taxes and the interest on your mortgage!

Add in the option to deduct expenses you incur for maintaining the property and you have the option to reduce your overall tax rate, which is always a good thing.

Some examples of expenses you can deduct

Labor for maintenance

Materials for maintenance

Depreciation

Gas if you drive to buy maintenance materials

Interest on you loan

There’s obviously a lot of tax benefits to owning property, which is why so many of the super wealthy people in this country own property.

Everyone wants to lower their income tax bracket, but that’s hard to do unless you own something. It can be property or a business, but if you don’t own anything it’s hard to make sizable deductions.

I’m not a tax expert (and you probably aren’t either) so you talk to your accountant to see what you could deduct.

Words of Caution

I still wouldn’t feel comfortable investing in a property without the ability to put at least 10% down.

You need to have enough savings left over to cover for vacancies and the inevitable maintenance costs that come with owning real estate.

Choose your property and the neighborhood you’re buying in carefully.

Neighborhoods that are mainly single family homes & commercial with a mix of multi-family properties are more attractive than neighborhoods with mainly renters.

Look at how the neighborhood is faring and how you think it will look in the future.

I’m all about holding real estate, so it’s important that neighborhoods I want to invest in continue to perform well into the future.

House hacking is all about reducing living expenses and if you splurge and can’t cover your payments you’re screwed.

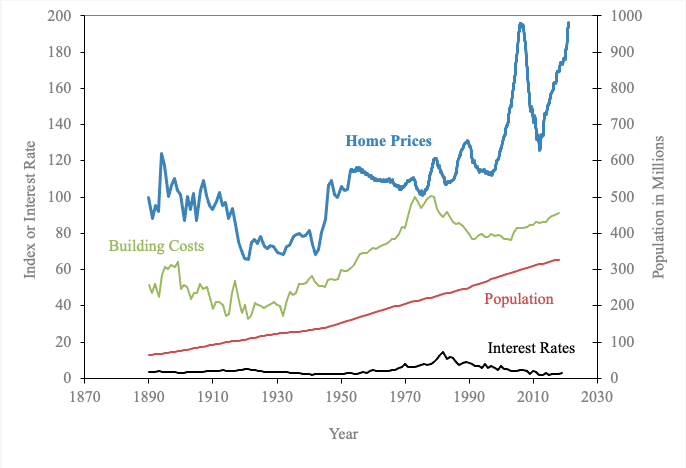

Housing prices are at a high that hasn’t been seen since 2008. I don’t have to remind you what happened the last time they were this high.

The Case-Schiller index looks at United States housing prices relative to the real home prices in 1890 (the value of 100 on the left y-axis for home prices).

Right now home prices are at almost 200. The real question is if this value is justified or just reflecting another bubble.

Thankfully I’m not in the financial position to even make that decision right now, but it’s important to think about for those of you who are.

Are you thinking about investing in real estate soon? Do you think house hacking is a good idea now? Let me know in the comments.

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

Your money would be much better served working for you in a 401(k) instead of splurging excessively. Let your money work for you in a 401(k).

Hint: You can also reduce your income taxes!

There are some splurges that absolutely kill my budget, but it seems like I can’t avoid them!

I love hanging out with my friends and meeting new people. Usually the best way to do that is to grab a couple drinks and something to eat. Maybe compete in a trivia game while I’m at it.

But I feel worse for wear when I check my bank account at the end of the week. Going out a couple times a week can wreck havoc on your budget. I want to take a look at three commons ways we tend to blow our budgets.

Just a disclaimer, I’m not advocating that we stay inside all day and never see friends. It’s important to know how much we spend on activities and constantly assess if we’re doing too much or too little. The pandemic has shown us that moments we spend together are meaningful, so it’s important to still make time for friends and loved ones.

I think a lot of impulse purchases include food because it’s easy to justify that we need food immediately whenever we’re hungry. It’s not our fault the deli is right there with their enticing aromas floating out of their door. I’m getting hungry just thinking about it!

Buying Breakfast & Coffee

Believe me I’ve been there. You wake up late and roll out of bed and realize that there’s no time to fry eggs and brew a pot of coffee. So you opt to stop at Starbucks or Dunkin on the way to grab a latte and a bagel.

A medium coffee from Dunkin is about $2.00 plus a bagel with cream cheese for another $2.00.

On a good week you only treat yourself with breakfast and coffee to-go twice. That’s $8.00 a week and it could be more if you want to get a breakfast sandwich or a latte.

Ordering Lunch

Once it rolls around to about noon I always have that familiar feeling in my stomach. No it’s not nerves, I’m hungry! It’s so much easier to just order lunch at work than it is to prep and remember to bring a meal from home.

The downside to ordering lunch everyday is that it can get expensive pretty quickly. Let’s say with delivery fees your lunch you love to order everyday is $15. That’s an extra $75 per week on eating out!

A cheap lunch from home like a sandwich or leftover pasta would probably cost $0.50 per portion at most. Ordering lunch is the difference between $75 per week and $2.50 per week.

Going Out For Drinks

Let’s look at the price of a beer in the United States. You’re looking at an average of around $4.50. Depending on where you’re at in the United States that could be on the low or high end for a beer at your local bar, but we’ll use that as a good reference price.

The average price is 45 cents more in New York City than for the entire USA, so I feel comfortable using $4.50 as our average price of a drink.

Don’t forget to be responsible and use an Uber if you don’t have a designated driver! Uber X fares from Midtown Manhattan to Soho with light traffic is about $18 but can go up to $45 with heavy traffic.

In my experience an Uber usually costs around $20 for my trips where I live during peak times.

You’ll likely be out for drinks after work at the same time as everyone else, so bet on paying that peak hour surcharge. I’m assuming you’ll probably split an Uber with friends so that brings the cost down too.

This brings your total for a night out to about$30 with a tip. This could be higher or lower depending on how far your Uber is, how many people split the Ubers, and how much you drink, but this is still a hefty amount.

If you go out twice a week thats $60 total to grab drinks with your friends.

What’s The Damage?

Let’s combine our weekly expenditures we looked at above to see how much we’ll spend each week

$8 for Breakfast/Coffee

$50 for Lunch

$60 for Drinks & Uber

Now we’re up to $118 per week on these splurges. That’s $472 per month, or $5,664 per year!

Either way this is a sizeable amount of money to spend on having fun. I’m not saying we shouldn’t have fun but there must be some other ways to have fun on a budget.

Investing In Your 401(k) Instead of Splurging?

One easy way to invest this money instead of spending it is in your 401(k).

In this example that’s a minimum of $6,000 per year (that’s awfully close to the amount we could splurge every year). Looking at the table below, you would have about $20,000 taxed at 22%.

$6,000 is pretty far from the 401(k)’s maximum annual contribution limit of $19,500. But even if you just invest half of the estimated $17,184 into your 401(k) you’ll be much better off. 401(k)s are a great tool to start saving for retirement and reduce your taxable income at the same time.

401(k)s allow you to put pre-tax earned income into an account where it can grow and be taxed when you take it out starting at 59 1/2 years old. The advantage of the 401(k) is that it reduces your current taxable income.

Source: Nerdwallet

If you invested about 10% into your 401(k) that would be $6,000. you would only have close to $14,000 taxed at 22% instead of almost $20,000. Thats the difference between $4,400 and $3,080 being taken out in federal income taxes. That’s just the federal income tax, expect to see more taken out if you live in a state or city with income tax.

I don’t know about you but I would much rather save $6,000 from being taxed and continue planning for financial success in retirement than go along without planning for my eventual early retirement.

Reducing my current income tax sounds great, but what if we looked at how much it can grow over time? We can assume an 8% long-term annual return in our 401(k). If we make consistent annual contributions of $6,000 to our account over 10, 20, or even 30 years the amount of money in that account will be a hefty sum.

How Your 401(k) Can Grow Over 10, 20, & 30 Years

Let’s look at your 401(k) growth if we assume an 8% return in your 401(k) and a contribution of 10% with a salary of $60,000.

After:

10 years you would have about $92,000.

20 years that grows into $296,000.

30 years your 401(k) will have a balance of $748,000!

This is all assuming no employer matching to your account. The power of compound interest is very real. It’s this opportunity makes me want to make sure I don’t splurge too much now.

If all I have to do is be a little bit more disciplined with my spending now in order to have a very comfortable nest egg in retirement, then I’ll do it without hesitation.

There is a debate on how much money you need in your retirement fund to comfortably withdraw in retirement, because inflation is very real and the power of one dollar will surely diminish over the next 30 years.

I like to allocate a 10% savings rate to a 401(k) because it’s fairly standard and hurts less than maxing out your 401(k) for people on a lower salary. The maximum annual contribution limit is currently $19,500.

The only problem is you need intense dedication to save this much pre-tax.

Plus you have to make sure you save at least 10% in post post-tax dollars.

Would you rather save more post-tax instead of pre-tax?

The more post-tax dollars you save, the sooner you will be able to buy real estate and diversify your income streams.

Regardless of how much you think you need in your account, there’s no doubt that saving pre-tax dollars in a 401(k) is a smart decision.

Let’s enjoy ourselves with our hard earned cash, but don’t forget to put some aside for retirement as well!

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.