With today’s inflation aggressively saving is not enough to retire comfortably. Learn what else you need to do.

When I was an undergrad I had a strategy professor who desperately tried to drive into my skull that cutting costs was never enough for a company to succeed; the first priority should be increasing revenue. This made sense but went against my instincts as everything in the supply-chain world was about cutting costs and increasing efficiency.

This is an essential concept in personal finance as well. Yes, we should be saving 50% of our income, but we won’t see any progress until we start to actively attempt to increase our salaries.

How to Increase Your Salary

Maybe the quickest way to increase your salary is to get a new job. It’s well known that job switchers receive pay increases that they simply would not have if they stayed at their current company. For whatever reason, loyalty to companies is not rewarded monetarily, never forget to look out for yourself!

If you want to stay at your current company look into educational opportunities that your company supports. It can be a master’s degree or certification. This can look different depending on your role and industry. Examples can include a 6 Sigma Blackbelt certification, or CFA/CPA designation. Master’s degree content can vary widely but almost always puts you in a position for an increase in responsibility, and therefore pay.

Pick up a side gig – some are easier to start immediately making money (think Uber and Lyft). Others like blogging take a lot of time usually without immediate results. That’s why driving for a ridesharing service is so popular there’s basically a guarantee that you will immediately start making money! Whatever you enjoy doing see if you can monetize that, streaming on platforms such as Twitch is incredibly popular. If you’re already gaming why not stream and try to monetize that?

It’s Not Easy

One reason increasing your salary isn’t talked about in personal finance circles is because it is hard. It takes a lot of effort, and you don’t see the payoff immediately. We can make instant impacts on our personal cash flow with budgeting and saving but most of us will be working the same job we’re in for probably another 2-3 years.

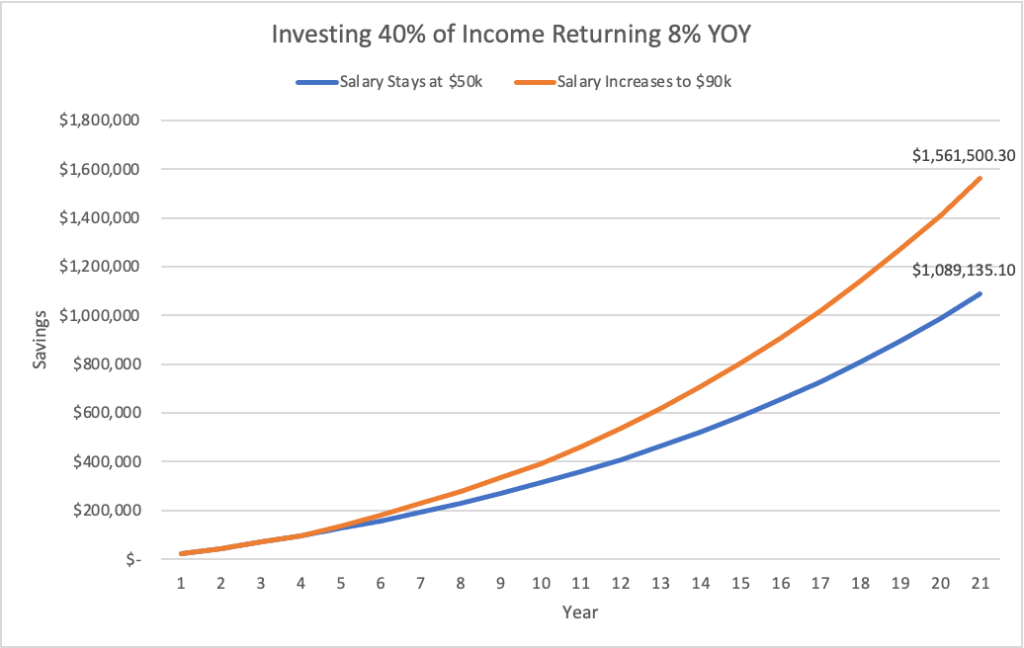

Here’s a way to visualize the difference between staying in one job and consistently investing assuming an average 8% rate of return on your investments. For simplicity’s sake, we’re not taking into account any investments that require larger capital outlays such as real estate purchases.

The person who consistently saves 40% of their $50,000 income could expect to have $1.09 million dollars after 21 years, that’s awesome! But take a look at the person who aims to increase their salary. They keep investing 40% of their salary but eventually reach a $90,000 income. They should end up with around $1.56 million dollars in invested savings. We’re talking about a difference of almost $470,000! With inflation currently around 9% in the USA, it’s probable to say $1 million won’t have the same purchasing power in 21 years as it does today. Every extra dollar earned and invested will help!

Drake is a freelance writer who’s interested in history, economics, art, & beer. He writes about popular personal finance topics and shares his personal finance experiences Make sure to check out more posts on Abnormal Money.

Ben Graham, the famous investor known for mentoring Warren Buffett and advocating for value investing, had a couple of brief rules for allocating your portfolio funds.

He has a simple rule depending on if you are an enterprising or a defensive investor.

How do you determine if you’re an enterprising or a defensive investor?

It’s not down to your age, but instead how much time you’re willing to put into managing your portfolio.

Enterprising vs. Defensive Investing

If you can’t really be bothered to take the time to properly value companies and invest in them, you’re a defensive investor.

You want to see your investments grow modestly without much effort.

If you get a lot of enjoyment from valuing companies and you want to spend the time to make these decisions in your portfolio then you’re classified as an enterprising investor.

Portfolio Allocations

Ben Graham advises that the enterprising investor limit his portfolio allocation to 75% in equities and 25% in bonds.

He advises that you never hold less than 25% of either bonds or equities.

You can rebalance your portfolio to be more or less conservative.

Graham’s argument for holding 25% of your portfolios in bonds is that it would give you the confidence to stay in the market whenever there is a market downturn.

An important note is that when Graham was writing his various editions of The Intelligent Investor US Treasury bonds were returning much more than they are today.

Portfolio diversity is an admission that you can’t select winning companies to invest in, which is okay.

Not everyone wants to dedicate the time and effort to learn how to evaluate companies and then consistently monitor them for investment opportunities.

But look at Buffett’s advice. Even when you buy the entire market through an index fund, he claims it’s best to place 90% of your portfolio in that one fund.

Sometimes diversifying can detract from our overall returns, especially if we diversify into high-cost equity funds.

How is your portfolio allocated? Would you consider yourself a defensive or enterprising investor?

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

You have time to incur losses and bounce back, so a reasonably aggressive approach would benefit your portfolio better.

Some Fund Managers Do Beat The Market

40% of managers do beat the market! That’s a large amount of funds to choose from.

Invest in these funds!

Do your research and identify the funds that regularly beat the market.

Keep in mind that past performance is not indicative of future results.

Anything can happen to your funds, and there is not a guarantee that any fund will continue to under or over perform the market.

Take the ARK funds as a recent example of a fund’s fortunes changing drastically.

It’s innovation fund TICKER: ARKK is down -17.94% at the time of writing compared to the S&P 500 index which is up +17.74% year-to-date.

Take the time to do your research and keep the amount of risk you’re taking on in mind.

Do not forget to check the fees that funds charge.

Funds that aim to beat the market often have huge fees, only to underperform a cheap index fund.

Actively Managing Your Own Investment Fund

Some people treat their investment accounts as their own fund.

They trade individual stocks and options instead of mutual funds & indexes.

This is obviously the most risky way to manage your money, as individual stocks are prone to much greater movements than larger funds.

Most people do not diversify enough with their individual holdings which leaves them overexposed in some industries and lacking exposure in others.

Mad Money Advice

Jim Cramer has solid advice on how to structure your investment account.

He suggests on investing your first $10,000 into a low cost index fund.

It’s important to look at a fund’s prospectus to understand the fees they charge, and also look at fee that your trading platform has on funds.

TD Ameritrade has a $49.99 charge on No-Load mutual funds as an example, which isn’t a big deal if you’re investing a couple grand but it is if you invest a couple hundred dollars.

After building up $10,000 in your index fund Cramer suggests keeping around 10 diversified individual stocks in your portfolio.

He claims this is a manageable number of companies that allows you to still keep up with quarterly and annual reports.

Options Trading

Options can get a little tricky, but there are two basic forms of options. Calls and puts.

Calls give you the option to purchase (call) or sell (put) a stock at an established price by a set deadline.

So with these options, its beneficial for you is a stock’s price increases with a call, since before the increase you’ve locked in a purchase price.

You essentially have the right to purchase shares for a discount from their market price.

The opposite is true with puts. You stand to benefit if a stock’s price goes down because you have the right to sell the stock for a price that is higher than it’s current market price.

A lot of trading of options happen, but it’s common for options to not actually be executed.

Options Trading Is Risky

For most part-time investors options are too risky of a strategy to effectively execute.

I would say they are one of the riskiest strategies available to most investors.

I got burned with options after initially having some success with them.

It’s important to remember that us casual investors are woefully under-informed compared to the massive institutions that execute thousands of complicated trades every day.

If you are interested in options make sure to do your research and really understand the risks.

Meme Stocks

You might have heard about “meme stocks” during the past year. One of the biggest has been AMC.

AMC was in financial trouble during the pandemic because lockdown restrictions were impacting their business model.

What short sellers were hoping would happen to AMC

Investors on Reddit saw that many of the large hedge funds and money managers were shorting (buying puts) on AMC.

Many of these Reddit investors were avid AMC customers, and were determined to not let their favorite movie theater franchise go out of business.

They started buying AMC en masse which drove the price of AMC up and screwed the short sellers because they now held options that were essentially worthless.

They had the option to sell AMC at a price that was below the market price, which of course no one wanted to exercise or buy the options.

What do you think? Do you prefer active or passive investment funds? Do you trade individual stocks? Are options a good long-term strategy? Let me know in the comments

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

Your money would be much better served working for you in a 401(k) instead of splurging excessively. Let your money work for you in a 401(k).

Hint: You can also reduce your income taxes!

There are some splurges that absolutely kill my budget, but it seems like I can’t avoid them!

I love hanging out with my friends and meeting new people. Usually the best way to do that is to grab a couple drinks and something to eat. Maybe compete in a trivia game while I’m at it.

But I feel worse for wear when I check my bank account at the end of the week. Going out a couple times a week can wreck havoc on your budget. I want to take a look at three commons ways we tend to blow our budgets.

Just a disclaimer, I’m not advocating that we stay inside all day and never see friends. It’s important to know how much we spend on activities and constantly assess if we’re doing too much or too little. The pandemic has shown us that moments we spend together are meaningful, so it’s important to still make time for friends and loved ones.

I think a lot of impulse purchases include food because it’s easy to justify that we need food immediately whenever we’re hungry. It’s not our fault the deli is right there with their enticing aromas floating out of their door. I’m getting hungry just thinking about it!

Buying Breakfast & Coffee

Believe me I’ve been there. You wake up late and roll out of bed and realize that there’s no time to fry eggs and brew a pot of coffee. So you opt to stop at Starbucks or Dunkin on the way to grab a latte and a bagel.

A medium coffee from Dunkin is about $2.00 plus a bagel with cream cheese for another $2.00.

On a good week you only treat yourself with breakfast and coffee to-go twice. That’s $8.00 a week and it could be more if you want to get a breakfast sandwich or a latte.

Ordering Lunch

Once it rolls around to about noon I always have that familiar feeling in my stomach. No it’s not nerves, I’m hungry! It’s so much easier to just order lunch at work than it is to prep and remember to bring a meal from home.

The downside to ordering lunch everyday is that it can get expensive pretty quickly. Let’s say with delivery fees your lunch you love to order everyday is $15. That’s an extra $75 per week on eating out!

A cheap lunch from home like a sandwich or leftover pasta would probably cost $0.50 per portion at most. Ordering lunch is the difference between $75 per week and $2.50 per week.

Going Out For Drinks

Let’s look at the price of a beer in the United States. You’re looking at an average of around $4.50. Depending on where you’re at in the United States that could be on the low or high end for a beer at your local bar, but we’ll use that as a good reference price.

The average price is 45 cents more in New York City than for the entire USA, so I feel comfortable using $4.50 as our average price of a drink.

Don’t forget to be responsible and use an Uber if you don’t have a designated driver! Uber X fares from Midtown Manhattan to Soho with light traffic is about $18 but can go up to $45 with heavy traffic.

In my experience an Uber usually costs around $20 for my trips where I live during peak times.

You’ll likely be out for drinks after work at the same time as everyone else, so bet on paying that peak hour surcharge. I’m assuming you’ll probably split an Uber with friends so that brings the cost down too.

This brings your total for a night out to about$30 with a tip. This could be higher or lower depending on how far your Uber is, how many people split the Ubers, and how much you drink, but this is still a hefty amount.

If you go out twice a week thats $60 total to grab drinks with your friends.

What’s The Damage?

Let’s combine our weekly expenditures we looked at above to see how much we’ll spend each week

$8 for Breakfast/Coffee

$50 for Lunch

$60 for Drinks & Uber

Now we’re up to $118 per week on these splurges. That’s $472 per month, or $5,664 per year!

Either way this is a sizeable amount of money to spend on having fun. I’m not saying we shouldn’t have fun but there must be some other ways to have fun on a budget.

Investing In Your 401(k) Instead of Splurging?

One easy way to invest this money instead of spending it is in your 401(k).

In this example that’s a minimum of $6,000 per year (that’s awfully close to the amount we could splurge every year). Looking at the table below, you would have about $20,000 taxed at 22%.

$6,000 is pretty far from the 401(k)’s maximum annual contribution limit of $19,500. But even if you just invest half of the estimated $17,184 into your 401(k) you’ll be much better off. 401(k)s are a great tool to start saving for retirement and reduce your taxable income at the same time.

401(k)s allow you to put pre-tax earned income into an account where it can grow and be taxed when you take it out starting at 59 1/2 years old. The advantage of the 401(k) is that it reduces your current taxable income.

Source: Nerdwallet

If you invested about 10% into your 401(k) that would be $6,000. you would only have close to $14,000 taxed at 22% instead of almost $20,000. Thats the difference between $4,400 and $3,080 being taken out in federal income taxes. That’s just the federal income tax, expect to see more taken out if you live in a state or city with income tax.

I don’t know about you but I would much rather save $6,000 from being taxed and continue planning for financial success in retirement than go along without planning for my eventual early retirement.

Reducing my current income tax sounds great, but what if we looked at how much it can grow over time? We can assume an 8% long-term annual return in our 401(k). If we make consistent annual contributions of $6,000 to our account over 10, 20, or even 30 years the amount of money in that account will be a hefty sum.

How Your 401(k) Can Grow Over 10, 20, & 30 Years

Let’s look at your 401(k) growth if we assume an 8% return in your 401(k) and a contribution of 10% with a salary of $60,000.

After:

10 years you would have about $92,000.

20 years that grows into $296,000.

30 years your 401(k) will have a balance of $748,000!

This is all assuming no employer matching to your account. The power of compound interest is very real. It’s this opportunity makes me want to make sure I don’t splurge too much now.

If all I have to do is be a little bit more disciplined with my spending now in order to have a very comfortable nest egg in retirement, then I’ll do it without hesitation.

There is a debate on how much money you need in your retirement fund to comfortably withdraw in retirement, because inflation is very real and the power of one dollar will surely diminish over the next 30 years.

I like to allocate a 10% savings rate to a 401(k) because it’s fairly standard and hurts less than maxing out your 401(k) for people on a lower salary. The maximum annual contribution limit is currently $19,500.

The only problem is you need intense dedication to save this much pre-tax.

Plus you have to make sure you save at least 10% in post post-tax dollars.

Would you rather save more post-tax instead of pre-tax?

The more post-tax dollars you save, the sooner you will be able to buy real estate and diversify your income streams.

Regardless of how much you think you need in your account, there’s no doubt that saving pre-tax dollars in a 401(k) is a smart decision.

Let’s enjoy ourselves with our hard earned cash, but don’t forget to put some aside for retirement as well!

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.