That makes buying used furniture an easy decision, especially if you’re not sure how long you’ll keep a piece of furniture.

I bought a set of Martinsville of America coffee tables and end tables for $120 at an estate sale a couple of weeks ago.

Buying used quality pieces can help keep you within your budget for furnishing your apartment.

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.

Liquid assets include things that can be easily accessed like checking & savings accounts, money market accounts, prepaid cards, and a few others. This amount has probably decreased due to COVID-19 limiting employment opportunities for many people.

Compare the number of liquid assets to the $44,390 median amount of total debt for the same group. That’s almost 14 times more debt than liquid assets!

I don’t know about you but that is a ratio I feel very uncomfortable with. The good news is that we can improve our financial health is by sticking to a planned budget.

Why

There are a couple of popular budgets to consider when planning your financial future. I’ll take a look at some by using the most recent figures for the real average personal income in the United States which was roughly $52,000 in 2019.

It’s important to note that this is significantly higher than the median personal income of $36,000, but it’s easier to use the average here because we will be using the average personal income tax rate of 22.4% when budgeting our post-tax dollars.

Below are three budgets that can help you get you spending under control. Using these budgets will surely increase your wealth in the long term.

Dave Ramsey’s Budget

Dave Ramsey has a proven method for budgeting called “zero-based budgeting”. To use this budget, we need to track where every dollar we make is going.

This intense focus on each category can be helpful for people who need a lot of structure but might be off-putting for others. Here is our budget using the average personal income in the United States.

Above are all 11 of Dave Ramsey’s budget categories and monthly/yearly contributions.

A lot is going on here but it’s important to note that the average income is reduced by $11,628 when we apply the average tax rate of 22.4%. That’s why it’s important to reduce your taxable income by saving your pre-tax dollars.

One issue I have with this budget approach is that some costs can vary a lot by geographic location. To live in a safe place near your workplace, you may have to spend more than 25% on your living expenses.

If you decide to use this budget template, make sure you keep the savings percentage at 10% at least when you’re adjusting other costs. This isn’t my favorite budget method, but I know it’s effective because of the success people have had with Dave Ramsey’s program.

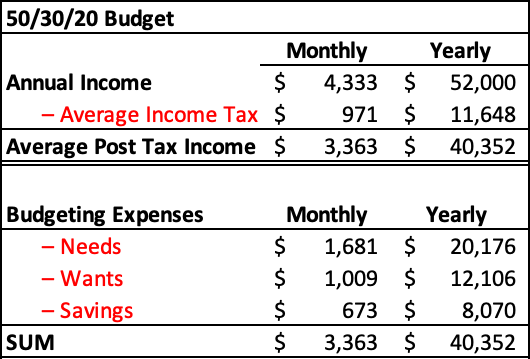

50/30/20 Budget

This budget was popularized by Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan. The appeal of this method is its simplicity. Instead of having to track eleven different categories like in Dave Ramsey’s plan, you only look at three general categories.

The breakdown of the 50/30/20 Budget. Pretty simple right?

We devote 50% of our income to needs, 30% to wants, and 20% to savings. This budget still requires setting aside time and go over your receipts or bank transactions and assign the transactions to these three broad categories.

It’s easier to keep track of this budget if you add expenses up as you go instead of sorting through every expense at the end of the month.

I like this budget because of its simplicity but some people may find they need more structure to keep them on a budget.

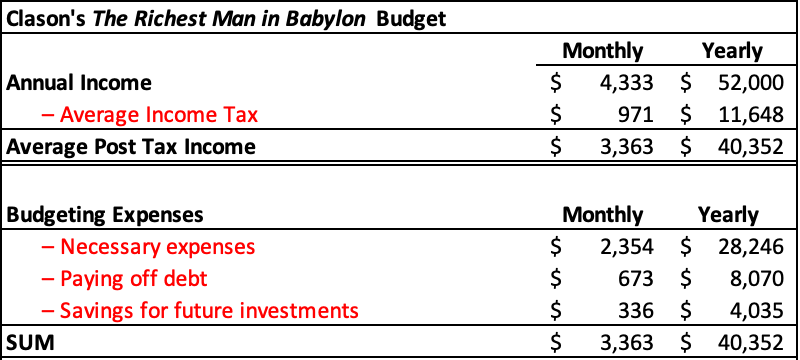

TheRichest Man in Babylon

The last budget we’ll look at comes from a book I read some years ago, George Clason’s The Richest Man in Babylon published in 1926. The book reads like a parable with a biblical inspiration set during the Babylonian empire.

The table below shows the budget outlined in the book:

Basically a 30% savings rate with a dedicated portion put towards paying down debt.

70% of personal income is allocated to necessary expenses, and the remaining 30% is split between using 20% to pay off debt and saving 10% with the goal of future investment.

This budget is nice because it explicitly provides a couple of implications for your budgeting.

You can set aside a portion of your 30% savings to pay off debt, and after that, this budget will look more like a 70/30 plan instead of a 70/20/10 plan.

If you have debt, you can use some of your savings in the other plans to pay that off too. It’s important to make investments to diversify your income streams and this budget makes sure that’s an explicit goal.

Investing should be a cornerstone of any budget. Make sure you understand why we should invest so you’re motivated and consistent.

Any Budget Is Better Than None

If you follow any of these budgets and you earn around the average income in the United States, you’ll have more liquid assets in savings than the median American under 35 years old after 5-9 months of saving.

It’s a great idea to keep your progress somewhere where you see it every day, whether that’s on your bathroom mirror or on your fridge.

Being constantly reminded of the progress you’re making will keep you encouraged as you start saving money and work towards financial independence!

Author Bio

Drake is a freelance writer who’s interested in history, economics, art, & beer. Drake graduated with a degree in Supply Chain Management and began working at General Motors. He writes about popular personal finance topics and shares his journey. Make sure to check back for more posts on Abnormal Money.